—–

Dividend Policy

—–

Investors

Dividend Policy

Group’s dividend policy is closely tied to the company’s earnings and future development outlook. According to Article 24 of its bylaws, after deducting previous losses and legal reserves, the distributable profit may be allocated—upon recommendation from the Board of Directors either to dividend distribution, retained earnings, or carry-forward

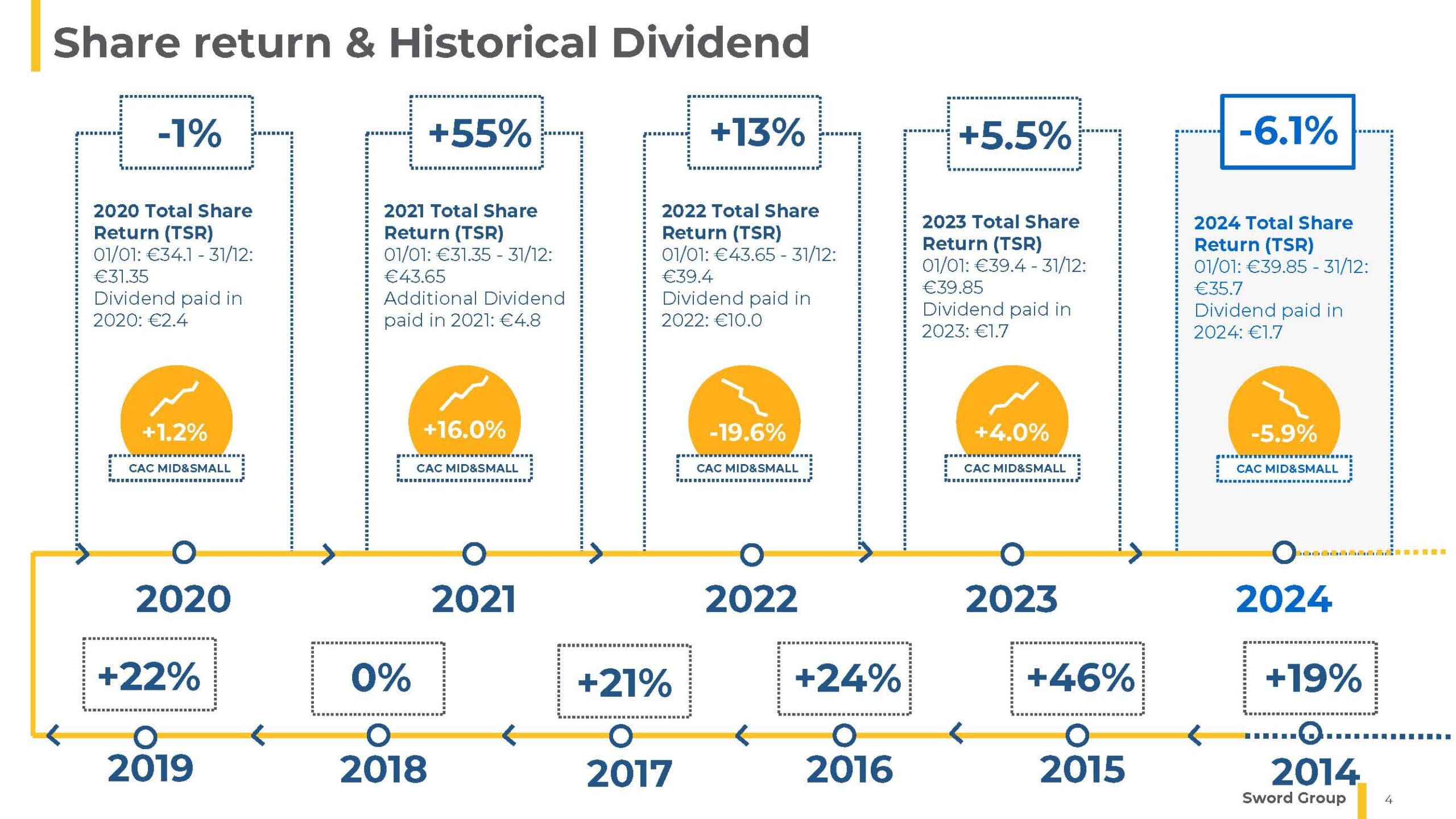

Historically, Sword Group has paid annual dividends, with amounts varying depending on the financial results of the fiscal year

- In 2022, an exceptional dividend of €10.00 per share was paid, reflecting extraordinary profits

- For the 2023 fiscal year, a dividend of €1.70 gross per share was proposed, with a payment date set for May 3, 2024

- Regarding 2024, subject to approval at the General Meeting on April 28, 2025, a dividend of €2.00 gross per share is expected, with an ex-dividend date of April 30, 2025 and payment on May 2, 2025

These decisions reflect Sword Group’s commitment to sharing its financial performance with shareholders, while also considering the investment needs required to support its continued growth

Upcoming Dividend

€2.0 gross per share

Ex-date: April 30, 2025

Record Date: May 2, 2025

Payment: May 5, 2025

Pending approval at the Annual General Meeting on April 28.

Dividends | Tax withheld at source

A natural person who is a shareholder and French resident for tax purposes

- If the shares are not placed on a PEA:

- The shareholder will benefit from a tax credit in France equal to the amount withheld at source => double taxation is avoided

- The IFU will mention the amount of the dividend and the amount of the tax credit

- If the shares are placed on a PEA:

- The tax credit cannot be refunded since the dividend is not taxed in France

A shareholder that is a legal entity established in France (with a holding of less than 10% and an acquisition price of less than 1.2 million euros

-

- The shareholder will benefit from a tax credit in France equal to the amount withheld at source => double taxation is avoided

A shareholder who is a natural person or a legal entity residing in a State other than France (with a holding of less than 10% and an acquisition price of less than 1.2 million euros)

-

- If the double taxation tax treaty between Luxembourg and the State of residence provides for a lower rate of tax withheld at source, the shareholder can file a request for partial or total reimbursement with the Luxembourg tax authorities (form 901bis)

- Moreover, in accordance with the tax treaty, the shareholder will benefit in his country of residence from a tax credit that is equal to the amount withheld at source => double taxation is avoided